The Year of the Intelligent Portfolio: Tax Strategy Meets Institutional Discipline

February 13, 2026

The most consequential investment decisions are rarely about predicting market direction. They are about designing systems that endure regardless of what markets do—systems informed by institutional discipline, tax intelligence, and the humility to acknowledge what we can and cannot control.

I had the privilege of presenting the 2026 Year-Ahead Portfolio Strategy for Fieldpoint Private Trust, LLC at TIGER 21 last month, and the response reinforced something I've long believed: sophisticated investors are not hungry for forecasts, but for frameworks. They want portfolios built with intention—where every allocation serves a purpose, where tax efficiency is structural rather than incidental, and where complexity is managed through clarity.

This is a reflection on how we are thinking about portfolio construction in 2026—and why the intersection of tax strategy and intentional design matters today.

The False Promise of Simplicity

There is an appeal to simple portfolios: a few index funds, some bonds, perhaps a real estate holding. For many investors, this approach has worked. But as wealth grows, as family structures become multigenerational, and as tax policy shifts with political winds, simplicity often becomes a liability disguised as virtue.

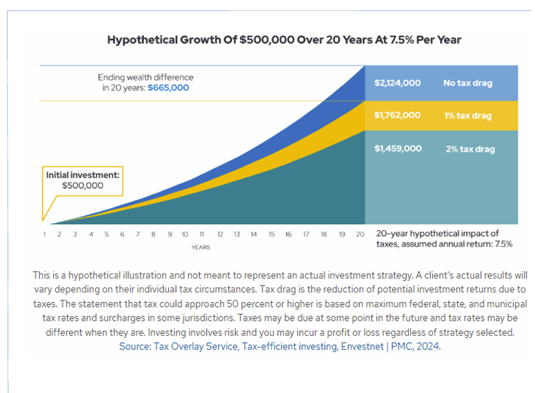

Large family portfolios increasingly resemble institutional portfolios—not just in scale, but in complexity, consequence, and time horizon. Decisions around asset allocation, liquidity, and taxes become more interrelated and more meaningful. A 2% difference in after-tax return, compounded over 20 years, can mean the difference between enduring generational wealth and generational collapse.

Research shows a hypothetical $500,000 portfolio growing at 7.5% annually would reach approximately $2.12 million over 20 years with no tax drag. With a 1% annual tax drag, that figure falls to $1.76 million. At 2%, it drops to $1.46 million.1 The difference—$665,000—is not a rounding error. It is a legacy either preserved or surrendered.

This is why we believe the most important asset allocation decision is not which stocks to own, but how to structure ownership in a way that tax efficiency becomes a structural advantage rather than an afterthought.

Cash Is Not Drag. It Is Protection.

One of the most persistent myths in portfolio management is that holding cash creates drag on returns. This is a false assumption—one that has destroyed more wealth than almost any other.

Every dollar in a portfolio has a job. Dollars allocated to cash reserves are not creating drag; they are creating protection. You accept lower returns in exchange for liquidity because illiquidity—not volatility—is the largest destroyer of wealth.

Consider the investor who, in 2008, was overallocated to private equity and real estate with insufficient liquidity to meet capital calls or cover spending needs. That investor was forced to sell public equities near their lows, locking in losses and forfeiting the opportunity to redeploy capital when markets recovered. The "drag" from holding 10% in cash would have been trivial compared to the permanent capital impairment from forced liquidations.

This principle is even more critical in 2026, as we navigate an environment characterized by:

Elevated equity valuations

Uncertain interest rate policy

Political volatility

In this context, liquidity is not a cost. It is optionality. It is the ability to act rather than react. It is the difference between deploying capital into dislocated markets and being forced to raise cash in them.

We Control the Tax Code, Not the Market

For many families, the largest controllable source of excess return is not manager selection but tax structure. Active managers may generate 50-200 basis points of alpha in a good year, and most fail to do so consistently. Meanwhile, thoughtful tax planning can reliably add 100-300 basis points annually with far greater consistency and lower risk.

This is what we call after-tax alpha—the systematic capture of tax benefits through structural portfolio decisions rather than one-off planning tactics.

Case Study: Tax-Intelligent Portfolio Restructuring

Consider a $25 million family portfolio generating substantial tax liabilities through a combination of W-2 income, business distributions, and investment returns. The family's marginal tax rate is 40.8% (37% federal + 3.8% net investment income tax), and they live in a state with an additional 6% income tax, bringing their combined marginal rate to approximately 46.8% on ordinary income and short-term gains.

Original Portfolio Structure:

$10M in actively managed mutual funds (60% equities / 40% bonds)

$8M in concentrated public equity position (low cost basis)

$5M in direct real estate holdings

$2M in cash and money market funds

Tax Leakage Analysis:

Mutual funds generate annual taxable distributions: ~$180,000 (1.8% of holdings)

Interest income from bonds and cash: ~$140,000

Short-term capital gains from active trading: ~$50,000

Total annual tax drag: ~$173,000 (approximately 0.7% of portfolio value)

After Tax-Intelligent Restructuring:

1. Municipal Bond Transition ($4M allocation)

2. Direct Indexing with Tax-Loss Harvesting ($6M allocation)

4. Private Credit & Real Estate Debt ($5M allocation)

5. Retained positions:

Concentrated equity position: Held in trust with charitable remainder unitrust (CRUT) structure to defer taxation and create income stream

Direct real estate: Maintained for depreciation benefits and 1031 exchange optionality

Annual Tax Impact:

Original structure: ~$173,000 annual tax burden

Restructured portfolio: ~$45,000 annual tax burden (net of harvesting and strategy benefits)

Annual tax savings: ~$128,000

After-tax return improvement: 51 basis points annually

Over 20 years, assuming 7% gross returns, this 51 basis point annual improvement would result in approximately $2.4 million in additional after-tax wealth, which is equivalent to adding 10% to the portfolio's ending value through tax structure alone.

This is after-tax alpha. This is what we mean when we say tax efficiency should be structural, not incidental.

Markets will do what markets do. We cannot control whether equities rise or fall, whether rates spike or subside, whether inflation persists or recedes. But we do have control over how the tax code informs our planning.

This is not about tax avoidance. It is about tax intelligence—structuring portfolios in ways that align legal and fiduciary obligations with long-term family objectives.

For tax-aware investors, this means:

1. Municipal bonds over taxable bonds to enhance after-tax income, particularly for high-net-worth families in states with elevated income tax rates.

2. Active tax-loss harvesting within public equity exposures, capturing losses to offset gains elsewhere in the portfolio.

3. Private investments structured to defer taxable events, supporting long-term compounding. Many alternative strategies—including private equity, venture capital, and real assets—generate returns primarily through long-term capital appreciation rather than ordinary income.

4. Hedging and hybrid strategies designed to generate tax benefits while providing portfolio stability.

These are not exotic strategies. They are applications of institutional best practices to family wealth—practices that endowments, foundations, and pension funds have employed for decades.

The Year-Ahead Portfolio: Positioning for Uncertainty

Our 2026 Year-Ahead Portfolio reflects a deliberate tilt away from crowded trades and toward areas of the market where we see structural value or differentiated risk-return profiles.

We are underweight public equities, particularly large-cap growth stocks that have dominated returns in recent years but now trade at elevated valuations. The so-called "Magnificent Seven" technology stocks have driven much of the S&P 500's performance, but concentration risk is now acute. When seven companies account for nearly 30% of the index, diversification becomes an illusion.

We are underweight traditional fixed income due to interest rate sensitivity. With government deficits persisting and inflationary pressures unresolved, we see limited upside in duration-heavy bond portfolios. Instead, we favor:

Private credit, where illiquidity premiums compensate investors for locking up capital

Real estate debt, particularly strategies focused on residential and multifamily lending

Floating-rate instruments that adjust with rising rates

We are overweight:

Small-cap equities, both public and private, which trade at more attractive valuations and may benefit from AI-driven efficiency gains

Commodities and private natural resources, which serve as inflation hedges and offer low correlation to traditional assets

Biotech, where we see multiple demand drivers—including aging demographics, AI-accelerated drug discovery, and more cost-effective research models

Hedging and alternative strategies, which provide portfolio stability and low correlation in place of traditional fixed income

This is not a bet on any single outcome. It is a portfolio designed to be durable across environments—resilient in downturns, opportunistic in dislocations, and flexible enough to adapt as conditions evolve.

Intelligent Design as Differentiation

At Fieldpoint Private Trust, we describe our approach as "Informed by Intelligent Design." This means emphasizing the intentional, purposeful structuring of wealth where all components work harmoniously.

Intelligent Design, in the context of portfolio management, means:

Every allocation has a purpose. Nothing is included by default or tradition. Every position is evaluated against its role in the broader portfolio.

Tax efficiency is structural, not incidental. We do not "add" tax optimization after the fact. We build it into the foundation.

Governance is clear and consistent. Roles, responsibilities, and decision-making authority are defined in advance, reducing the likelihood that emotional or ad hoc decisions will undermine long-term outcomes.

Liquidity is managed proactively. We stress-test portfolios under adverse conditions, modeling liquidity needs across capital calls, spending requirements, and rebalancing obligations.

This discipline is not glamorous. It does not generate headlines or inspire breathless predictions. But it is what endures.

Governance: Where Most Portfolio Mistakes Begin

Many portfolio mistakes are actually governance mistakes in disguise. Families that lack clear decision-making authority, spending policies, or role definitions often find themselves making reactive, suboptimal choices during market stress.

Consider the family that sells equities near market lows because different family members have different risk tolerances and no one had documented decision-making authority in advance. Or the family that over commits to private investments because there was no formal liquidity policy, only general agreement that "alternatives are good for diversification."

Governance failures manifest as portfolio problems:

Excessive trading from unclear authority and conflicting opinions

Overallocation to illiquid assets from inadequate cash flow modeling

Concentrated positions held too long from emotional attachment rather than rational analysis

Missed opportunities from slow decision-making during market dislocations

For multigenerational families, governance becomes even more critical. The founder may have built wealth through concentrated risk-taking and intuitive decision-making. The next generation may need systematic frameworks to steward that wealth that extend decades beyond any individual's involvement.

Governance design is a significant consideration when it comes to helping families build decision-making structures that outlast any single advisor, family member, or market cycle.

A Fiduciary Commitment

This is our calling. Not to chase returns. Not to time markets. But to serve as stewards—balancing the needs of today with the obligations of tomorrow, managing complexity with clarity, and building portfolios designed to endure across generations.

The most intelligent portfolios are not the most complex. They are the most intentional. And in 2026, intention matters more than ever.

__________________________________________________________________________________________________________________________________________________________________

Sources:

Parametric Portfolio Associates, "The Tax Benefits of Direct Indexing," 2023. Study analyzed 1,000 simulated direct indexing portfolios from 2001-2020, finding average annual tax-loss harvesting benefits of 1.0%-2.0% for high-net-worth investors in the highest tax brackets. Actual results vary significantly based on market conditions, cost basis, and individual tax circumstances. Read for more.

Disclosures:

This article is for informational purposes only. It is not intended as, and should not be construed as, legal, tax, investment, or accounting advice. The information contained herein is general in nature and does not take into account specific investment objectives, financial situation, or needs. Nothing in this article constitutes a recommendation, offer, or solicitation for the purchase or sale of any security, trust service, or investment product.

The allocation presented here is subject to change and based upon market conditions and the objective of the portfolio. Each client portfolio is managed on a unique basis, so the percentages allocated to a particular asset class may vary by client. Please contact your Advisor to complete an updated risk assessment to ensure that your investment allocation is appropriate.

Fieldpoint Private Trust does not provide investment, legal, or tax advice unless expressly agreed to in writing through a separate client agreement. Any references to investment managers, custodians, or products are for illustrative purposes only and do not imply endorsement or assurance of future results. Investments, including private funds and alternative strategies, carry risks, including the potential loss of principal. Past performance is not indicative of future results.

Trust services are provided under the regulatory framework applicable to trust companies and are distinct from the services of registered investment advisers and broker-dealers. While every effort has been made to ensure the accuracy of the information presented, Fieldpoint Private Trust makes no representation or warranty as to the completeness or accuracy of the content herein and assumes no obligation to update or revise it.

Trust services offered through Fieldpoint Private Trust, LLC, a public trust company chartered in South Dakota by the South Dakota Division of Banking.